Diversifying beyond the services sector and boosting investment in agriculture and manufacturing, especially processing industries, can help India attract stable and long-term FDI inflows

Published Date – 6 April 2026, 10:59 PM

By Abhinav BJ, Lakshya Bhownani, Dr Kedar Vishnu

Due to rising global uncertainty, driven by war between the United States, Israel, and Iran, ambiguity surrounding the US trade deal, and ongoing supply chain disruptions, the flow of foreign direct investment (FDI) has been significantly affected, particularly in India. Over the last few years, India has put greater emphasis on raising per capita income by expanding trade and boosting manufacturing through higher FDI inflows.

Negative net FDI inflow

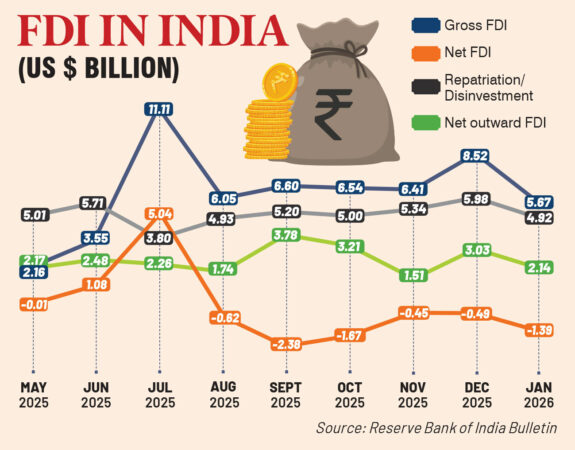

According to RBI data, net FDI in India remained negative for the fifth consecutive month, recording –$1.39 billion in January 2026, compared to –$0.49 billion in December 2025. The decline in India’s net FDI is mainly driven by a sharp increase in repatriation and a decline in fresh inflows. While gross FDI inflows dropped from $8.5 billion in December 2025 to $5.7 billion in January 2026, repatriation/disinvestment remained high at $4.9 billion in January 2026, resulting in a negative net FDI inflow.

More concerning than declining gross inflows is the rise in repatriation/disinvestment. The movement is largely explained by a disinvestment of approximately $5 billion over the past few months, and January 2026 recorded outflows of $4.8 billion. This means that most of the foreign investors are selling their stakes in the Indian company and taking profits back to their home countries. Foreign investors are seeking more profitable and attractive companies abroad and safer global investment opportunities.

Similarly, Indian firms have been investing more abroad. In January 2026, net outward FDI stood at $2.14 billion, and the trend has continued, showing Indian companies’ interest in global markets. A key driver of this figure was equity capital, which stood at $1.62 billion in January 2026, reflecting a surge in Indian companies’ investments in foreign assets, possibly through acquisitions or new partnerships.

Reinvested earnings remained stable at $0.64 billion, which has been consistent for the last few months, reflecting that Indian businesses are still generating profits from their overseas operations and the firms have been reinvesting abroad for future expansion. Meanwhile, the repatriation/disinvestment component rose sharply to $0.53 billion, up from $0.22 billion in December 2025, suggesting greater capital withdrawals from foreign ventures.

These outflows will have several adverse impacts on the Indian economy in the short run, leading to a shortage of capital for domestic investments. Further, disinvestment will further depreciate our currency as the supply of rupees increases in our economy, further eroding its value.

Increased outward FDI by Indian firms, particularly in the form of equity capital, can be beneficial if the investment eventually returns with improved technology and enhanced experience gained from operating in competitive, developed markets. The increase in FDI outflows reflects Indian companies’ growing focus on global expansion, alongside foreign investors repatriating profits. Around 75 per cent of outward FDI flows were directed to the US, Singapore, the UK, and the UAE during April 2025–January 2026.

Developed countries have accounted for 45% ($728 billion) of global FDI inflows in 2025, while developing countries attracted the remaining 55% ($877 billion), underscoring their growing importance as investment destinations. There has been a shift in FDI allocation from developing to developed countries. Further investment is becoming more concentrated in a few capital-intensive sectors, particularly data centres.

Who is investing in India?

India’s share of global FDI inflows declined to 1.83% in 2024 from a peak of 3.55% in 2022, reflecting a broader global slowdown and tighter financial conditions. Looking at the share of the top investing countries in India, Singapore has strengthened its dominance, rising from 26.50% in 2023–24 to 36.87% in 2025–26 (Apr–Dec).

Similarly, the US share has also increased from 11.25% to 16.31%. On the other hand, Mauritius saw a sharp decline from 17.94% to 10.09%, and the Netherlands from 11.08% to 4.80%, partly due to regulatory changes after 2020 and reduced tax advantages. Japan remained relatively stable, moving from 7.15% to 6.68%, while the UAE rose to 8.69% in 2024–25 before easing to 5.13%.

Notably, smaller contributors such as the Cayman Islands increased from 0.77% to 4.12%, and Cyprus from 1.81% to 2.94%, indicating diversification in investment channels. Overall, the data highlights a shift away from traditional FDI sources towards a more concentrated, yet evolving set of investors led by Singapore.

Increasing FDI

The Union cabinet removed the requirement for FDI approval and eased norms for all countries that share land borders with India in March 2026. Earlier, China, Bangladesh, Bhutan and other countries were required to obtain government approval under the automatic route.

In 2020, the government imposed several restrictions to prevent ‘opportunistic takeovers’ of Indian companies by Chinese firms following the Ladakh conflict. Allowing up to 10% FDI without government approval could ease investment flows. Increased FDI would help attract more investment in the manufacturing of electronic capital goods, electronic components, polysilicon, and ingot-wafers.

The Indian government is also holding inter-ministerial consultations to raise the FDI limit for state-run banks from 20% to 49%. As of now, India has allowed 74% of FDI in private banks through shareholding by any single foreign institution, subject to a cap of 15% unless the RBI grants a specific exemption. This move would help the government attract more capital and boost investment in the banking sector.

Additionally, the Department for Promotion of Industry and Internal Trade (DPIIT) has held a series of meetings with various stakeholders to boost FDI in India. However, despite the government’s increased focus in recent times, the trend of negative net FDI over the past five months has not yet been reversed.

The government needs to establish a robust institutional mechanism to attract more FDI to manufacturing and rural areas. Major reforms are needed to improve the ease of doing business, government effectiveness, and the rule of law to make the FDI process much faster, smoother, and more efficient. Also, we need to attract more FDI into much-needed sectors like agriculture and the processing industry, rather than focusing solely on the services sector.

(Abhinav BJ and Lakshya Bhownani are students of Economics and Political Science, while Dr Kedar Vishnu is Associate Professor at the Manipal Academy of Higher Education [MAHE], Bengaluru)