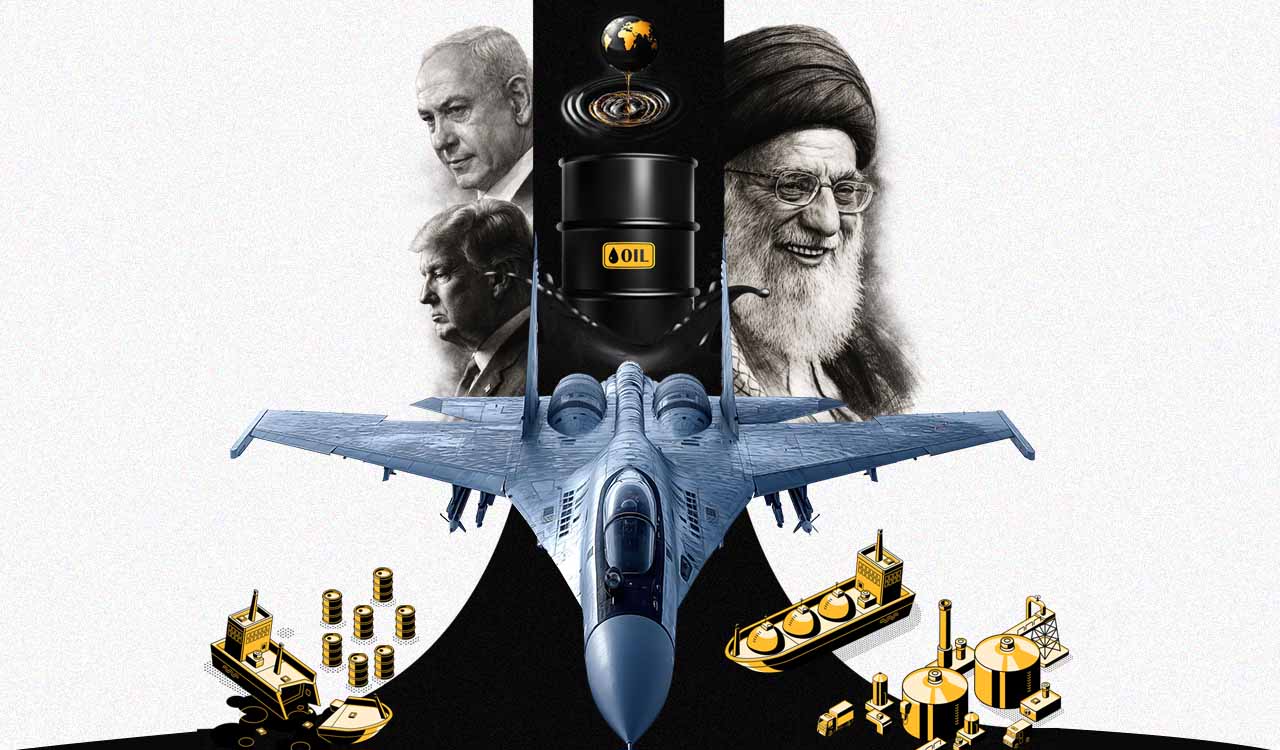

Escalating tensions around the Strait of Hormuz following the US–Israel conflict with Iran are rattling global energy markets, exposing Asia’s heavy dependence on Gulf oil

Published Date – 7 March 2026, 10:56 PM

By Dr Anudeep Gujjeti, Dr Tania Anupam Patel

Wars in West Asia are often narrated as clashes of ideology, deterrence, and regime change. But oil markets narrate them differently — as a contest over credible threat to sea lanes, terminals, refineries, insurers, and the willingness of commercial shipping to accept risk. That is why this Iran war has produced an energy shock, even before the world can agree on what the closure of the Strait of Hormuz means.

As of March 5, 2026, the war’s energy signal is already clear: Brent is at $84.32 per barrel, and US crude (WTI) is trading above $78, up more than 43% since December amid prolonged near-halt conditions around the Strait of Hormuz. Moreover, the shock is not confined to crude oil. Stress in refined products, such as diesel, or in freight and insurance channels, considered “secondary” transmission mechanisms, can turn a regional war into global inflation.

The situation is fast-moving and, on some fronts, difficult to independently verify in real time. Yet the market does not require perfect information: it requires only a plausible pathway to disruption. In this war, that pathway is clear. Many oil and gas facilities in the Gulf have been attacked, including the UAE’s Fujairah and Mussafah oil terminals, Qatar’s Ras Laffan Industrial City LNG facilities and Saudi Arabia’s Ras Tanura oil refinery. While this is ongoing, the region has a long history of oil crises.

Turbulent History

The foundations of the modern Iranian oil industry were laid by the Consortium Agreement of 1954, which followed the 1953 coup orchestrated by the United Kingdom (UK) and the United States (US) to overthrow Iranian Prime Minister Mohammad Mossadegh after he attempted to nationalise Iranian oil.

This agreement divided Iranian oil ownership among a consortium of Western firms: 40% to five American majors (Exxon, Mobil, Socal, Texaco, and Gulf), 40% to British interests (Anglo-Iranian, later BP), 14% to Royal Dutch Shell, and 6% to the CompagnieFrançaise des Pétroles. The framework integrated Iran into the Western economic orbit for 25 years, granting the United States and Britain significant influence over production levels and global pricing until the 1979 Revolution.

• The 2026 crisis echoes the 1980s Tanker War but goes further: Operation Epic Fury marks a direct US combat role, shifting strategy from deterrence to open hostility

The 1979 Iranian Revolution abruptly dismantled the Western-backed oil order in Tehran and introduced a revolutionary regime that unsettled the regional balance of power, prompting Iraq’s invasion in September 1980 and setting the stage for the protracted Iran–Iraq War, which would eventually spill into the Persian Gulf’s shipping lanes.

The Tanker War (1980–1988)

The current disruption of shipping in West Asia draws immediate parallels to the ‘Tanker War’ phase of the Iran-Iraq War. During that conflict, both states targeted commercial vessels to degrade each other’s economic capacity. Between 1980 and 1988, approximately 2-5 million barrels per day (mb/d) of production were taken offline at various stages, contributing to sustained price volatility throughout the decade.

The crisis of the 1980s prompted the United States to initiate Operation Earnest Will, the largest naval convoy operation since World War II, to escort reflagged Kuwaiti tankers through the Strait of Hormuz. While the current 2026 crisis shares certain characteristics with the 1980s, such as the mining of the strait and attacks on tankers, the intensity of ‘Operation Epic Fury’ is markedly different. Unlike the 1980s, when the US was not a direct combatant for much of the conflict, the 2026 strikes represent an overt regime-change strategy that has fundamentally shifted the threshold from calibrated deterrence to declared hostility.

Strait of Hormuz

The Strait of Hormuz remains the world’s most critical energy chokepoint, a geographic bottleneck connecting the Persian Gulf to the Arabian Sea. Approximately 167 km long and only about 33 km wide at its narrowest point, between Iran and the Musandam Peninsula, the strait has shallow waters near the coast that constrain navigation. As a result, tankers must pass through two shipping lanes, approximately 3 km wide, one in each direction, separated by a 2 km buffer zone. What we are witnessing through the functional closure of the Strait of Hormuz is a commercial deterrence rather than an outright military blockade.

In 2024, approximately 20 million barrels per day of petroleum transited through the strait, representing roughly 20% of global petroleum consumption and over one-quarter of global seaborne oil trade. The West Asia Gulf supplies approximately 20% of global seaborne LNG. Moreover, the region also accounts for 16-18% of global seaborne fertilizer exports. LNG shipments through the Strait of Hormuz have been suspended since February 28. West Asia LNG flows predominantly serve Asia.

In January 2026, West Asia accounted for 55% of India’s crude imports, about 2.74 million barrels per day, partly because Russian imports eased relative to their earlier peaks. As far as LNG is concerned, India sources around two-thirds of its supply from Qatar, the UAE, and Oman. This concentration becomes especially consequential because LNG cargoes are logistically rigid and contract-linked. Recently, GAIL mentioned that India’s LNG suppliers have issued a Force Majeure notice, a legal clause in contracts through which exports can be stopped due to extraordinary events beyond the control of the parties.

Japan is Asia’s classic case of Gulf exposure: about 90% of its oil imports come from West Asia, along with 11% of its LNG imports. Including both national stockpiles and private inventories, Japan has reserves sufficient for around 254 days.

South Korea’s energy basket is more hybrid in nature—not as oil-concentrated as Japan’s, but still heavily exposed. South Korea imports roughly 70% of its oil and about 20% of its LNG from West Asia. In December last year, South Korea’s Industry Ministry said the government’s strategic petroleum reserves had reached 100 million barrels, with the private sector holding another 95 million barrels. This week, South Korea announced that, taken together, these stocks would cover roughly 208 days of national consumption.

• After the 1953 US-UK-backed coup against Iranian Prime Minister Mohammad Mossadegh, the 1954 Consortium Agreement divided Iranian oil among Western firms, binding Iran to Western economic influence

China sits in a different category. It is deeply dependent, but more insulated by scale and storage. Half of China’s oil imports, and about one-third of its LNG comes from West Asia, large enough to shape national energy planning, but cushioned by broader supplier optionality and large strategic commercial inventories of three months or around 900 million barrels.

Geopolitics of Escalation

The conflict this time appears different for Asia, given the region’s greater dependence on Gulf oil compared to earlier crises in the 1970s and the early 2000s during the Iraq War, when the Strait of Hormuz remained open, and supply chains were largely unaffected. First, the crisis has triggered an insurance-led shutdown, with insurers and shipping firms concluding that the waterway’s narrow S-shaped route is too risky to traverse. The Iranian Mission to the United Nations has reiterated its commitment to international law and freedom of navigation, dismissing claims about closing the Strait of Hormuz as baseless, thereby amplifying the narrative battle.

Nevertheless, the reverberations of the escalating costs have already been felt by the US. To address the energy crisis faced by Asian countries, many of which are its allies, the US has heeded the pressure. President Donald Trump posted on Truth Social that the US Development Finance Corporation (DFC) will provide insurance at a “reasonable price” to ensure maritime energy trade, along with a promise of US naval escorts for tankers if necessary.

This comes in light of the sharp escalation in premiums charged by freight and marine insurance companies, which have risen to nearly 80% due to war-risk exposure. In addition, the withdrawal of marine hull war-risk coverage has imposed further costs on the global supply chain as the situation continues to escalate. To protect European energy interests, France has already promised to deploy two additional ships to the Aspide mission, which includes vessels from France, Italy, and Greece tasked with protecting shipping in the Red Sea and the Gulf of Aden.

Second, Asia today, lies at the centre of global energy demand, driven by its rapidly growing population and the accompanying rise in consumption needs. This vulnerability is further intensified by the region’s heavy dependence on long-distance maritime supply routes that pass through various chokepoints, with the Strait of Hormuz being an important one. Consequently, Asian markets—whose energy sources are less diversified compared to those of other regions—remain particularly exposed to supply disruptions, deepening economic vulnerability.

The US also gave India a temporary 30-day waiver period to purchase Russian oil, noting that this waiver does not generate any substantial financial gains to the Russian government, as this is limited to oil shipments stranded at sea. However, this should not be seen as an act of benevolence, but as a strategic move giving the US extra time to pursue regime change and use the outcome to its advantage in the domestic political arena under Donald Trump.

The unfolding escalation in West Asia represents a multidimensional geopolitical and economic risk event. Although oil markets remain the most visible barometer of this crisis, the ramifications across insurance, aviation, and global trade corridors are equally significant. The ‘Tanker War’ of the 1980s proved that the energy market can adapt to prolonged supply uncertainty. However, the scale and intensity of the current ‘Operation Epic Fury’ suggest that history is not merely repeating itself but also evolving into a more existential form of confrontation.

For India, maintaining a diversified supply portfolio, particularly with Russia and non-Hormuz producers, and expanding strategic petroleum reserves will be essential to mitigating risks associated with the “effective closure” of the world’s most critical energy artery. The present crisis underscores the urgent need for geographically diversified supply chains and accelerated investment in renewable energy to reduce structural vulnerability to external geopolitical shocks.

(Dr Anudeep Gujjeti is Assistant Professor, Symbiosis Law School, Pune, and Young Leader, Pacific Forum, USA. Dr Tania Anupam Patel is Assistant Professor, Symbiosis Law School, Pune)